Educational guidance — not a substitute for advice from your CPA or audit firm.

For a lot of nonprofit finance teams, June 30 arrives the same way every year: like a deadline you knew was coming but somehow still feels sudden. The meeting requests stack up. The auditor sends a list. Someone on the program team asks if a grant expense "made it in" before close. And whoever manages the books is expected to hold it all together while running the rest of the month.

It doesn't have to be this way. A chaotic year-end close isn't inevitable — it's usually the result of a missing process, not a missing person. Organizations that close cleanly aren't better staffed. They're better prepared.

This guide gives you a clear, step-by-step process for closing your June 30 fiscal year with accurate books, a calm audit, and a board that understands what happened. No heroics required.

Why the Year-End Close Matters More Than You Think

It's a Compliance Document AND a Reputation Document

Your year-end financial statements aren't private. They feed your Form 990, which is publicly available. They're what auditors test, what funders review, and what board members rely on to understand the health of the organization. A clean year-end close is a form of organizational credibility — it tells the people who depend on your financial statements that your organization has its act together.

What Happens Downstream When the Close Is Messy

The consequences of a disorganized close compound quickly. Delayed financial reporting means your board can't make informed decisions before the new fiscal year begins. Audit adjustments extend the audit timeline, increase fees, and can result in a management letter comment that funders and oversight bodies will see. Restricted fund errors are particularly costly — they're not an accounting problem, they're a compliance problem with the funder.

How to Set Up Your Close Before the Deadline Hits

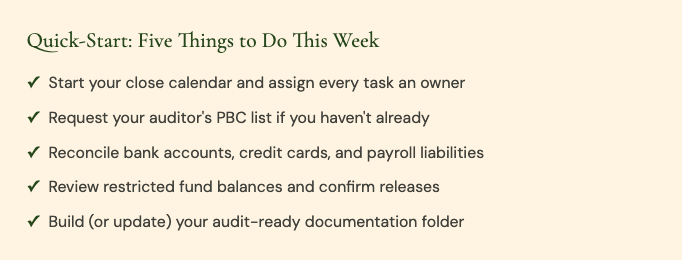

Build Your Close Calendar and Assign Owners

Ambiguity is the enemy of a clean close. Build a one-page close calendar with every task, a responsible owner, and a deadline. Include the small things: who sends the auditor's engagement confirmation, who collects board-signed policy confirmations, who follows up on outstanding invoices before cutoff. A close calendar isn't bureaucracy — it's the thing that lets your team close in two weeks instead of six.

Get the Auditor's PBC List Early — What It Is and Why It Matters

PBC stands for "Prepared by Client" — it's the list of schedules, documents, and reconciliations your audit firm will expect when fieldwork begins. Request it 6–8 weeks before your audit start date. Some items on the list will reveal gaps in your current recordkeeping. Getting the list early gives you time to prepare rather than react.

Target Your Final Close Within 60–90 Days of June 30

Aim to have your books fully closed and your audit-ready package ready within 60–90 days of year-end — a clean close by late August at the latest, with audit fieldwork beginning in September for most organizations on a June 30 year-end.

The 7-Step Year-End Close Process

1. Reconcile the "Big Three": Bank, Credit Cards, Payroll Liabilities

Start here. If your bank accounts, credit cards, and payroll liability accounts aren't reconciled and tied out, everything downstream is built on uncertain ground. Don't just reconcile to a zero variance — review items in transit or outstanding. Old uncashed checks may need to be voided and potentially treated as unclaimed property.

2. Clean Up AR and AP

For receivables: Are outstanding pledges actually collectible? Are reimbursement grant receivables supported by expense documentation? For payables: Are there invoices for services delivered before June 30 that haven't been entered yet? Those need to be accrued. Your balance sheet should reflect what you actually have, not what you hope to have.

3. Review and Confirm Restricted Funds and Grants Before You Close

Before closing the books, confirm for every restricted fund and active grant: What are the restrictions? What was spent against those restrictions this year? What releases should be recorded? What balance carries forward? Do this before you close. Reconstructing it after the fact is far more painful.

4.Check Revenue Recognition, Especially for Grants

Recognize grant revenue when conditions have been met, not necessarily when the cash arrives. A grant check received in May for a program starting in July should not be recognized in May. A grant for which conditions were met by June 30 should be recognized in the current year, even if the reimbursement request hasn't been submitted. Review each active grant agreement before close.

5.Review Fixed Asset Additions and Depreciation

Confirm all equipment purchases and capitalized expenditures for the year are properly recorded. Record or confirm depreciation for the full year. If any assets were sold or taken out of service, record the disposal and any gain or loss.

6.Run and Review Your Final Financial Statements

Once all adjustments are posted, generate your full set of financial statements: Statement of Financial Position, Statement of Activities, Statement of Cash Flows, and Statement of Functional Expenses. Review them before sending them anywhere. Look for unexpected year-over-year swings and unusual ratios. Your auditors will notice these — you want to notice them first.

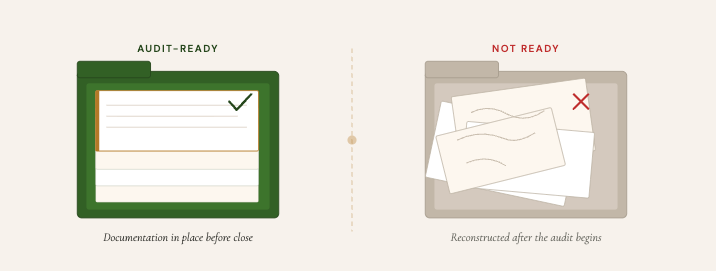

7. Build Your Audit-Ready Folder

Even organizations not subject to a formal audit benefit from building an audit-ready folder — an organized package of supporting documentation. This includes bank reconciliations, grant award letters, depreciation schedules, payroll summaries, board meeting minutes, documentation of your functional expense allocation method, and policy confirmations. Building this folder annually makes you genuinely audit-ready and protects against institutional knowledge loss when staff transitions occur.

Three Year-End Close Mistakes That Create Audit Problems

Mishandling Restricted Fund Releases — The Most Common Audit Finding

Restricted fund releases need to be recorded in the period when the restriction was satisfied. Recording them in the wrong period distorts both your Statement of Activities and your net asset balances. The fix is tracking restrictions actively throughout the year, not reconstructing them at close.

Revenue Recognition Timing Errors on Grants

This shows up in two directions: recognizing revenue too early (before conditions are met) or too late (after conditions were met but the close was delayed). The protection is reviewing each grant agreement before the year closes. Confirm the type of grant, the conditions attached, and the period of performance. When in doubt, involve your accountant before the close — not during audit fieldwork.

Waiting Until After June 30 to Start — The Cutoff Problem

Cutoff means revenues and expenses need to be recorded in the period they were earned or incurred, regardless of when cash moves. A vendor invoice for services delivered in June but received in July still belongs in June's books. Waiting until July to start thinking about year-end means you're already behind on the cutoff work. The close calendar exists to prevent this.

The Post-Close Leadership Review: Where Finance Becomes Strategy

Year-Over-Year Comparison: What Changed, What Needs a Narrative

Pull your current-year financial statements alongside last year's. Look for significant year-over-year swings. These aren't problems — they're data points. But they need narrative explanations, both for your board and for the auditors who will ask about them. Document the explanations now, while the context is fresh.

What to Bring to Your Board Before the Audit Starts

Your board meeting before the audit is your opportunity to set expectations and surface any items that warrant board awareness before auditors arrive. Share your draft financial statements, a year-over-year summary, any significant accounting judgments, and a projected audit timeline. A short pre-audit board briefing builds confidence and reduces mid-audit surprises.

When to Bring In Outside Help

For many nonprofits, the year-end close is manageable with existing staff when the process is clear and the monthly closes have been kept current. But there are situations where outside support makes a real difference: your books are multiple months behind heading into year-end, you have complex restricted fund structures, you're going through your first audit, or a key staff member has left and the institutional knowledge left with them.

If any of those situations describe where you are this June, Financial Affairs works exclusively with nonprofits on exactly this kind of close and audit preparation support.

Download the Year-End Close & Audit Prep Checklist

A step-by-step checklist with a 30-day close calendar, reconciliation tracker, restricted fund closeout checklist, and a PBC starter list.

A Clean Close Is a Leadership Act

The year-end close is the moment when a full year of financial activity becomes the official record of your organization's stewardship. When that record is accurate, organized, and well-supported, it tells a true story — one your board can stand behind, your auditors can verify, and your funders can trust.